The world currently has 8.2 billion people and a global economy approaching $120 trillion. The world also routinely experiences extreme weather events like tropical cyclones, floods, and tornadoes. [1]

Given these facts, how much economic loss should we expect annually from extreme weather events in the context of the global economy?

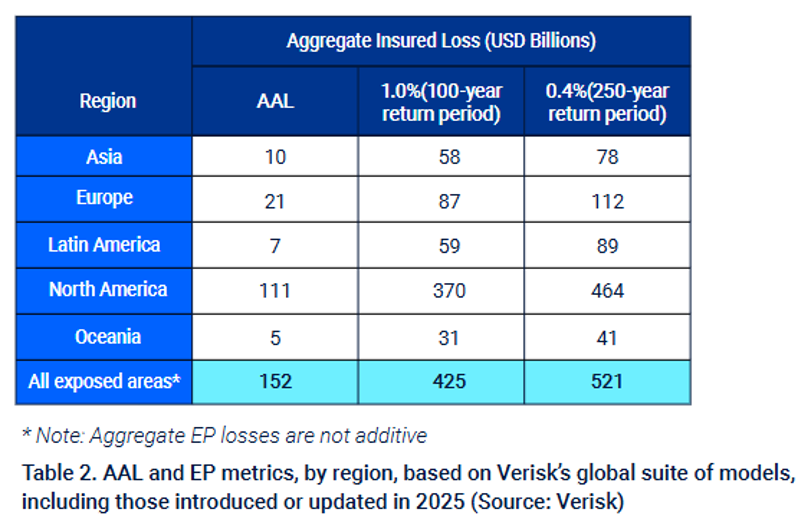

For 2025, the catastrophe modeling firm Verisk provided their estimate [2] — $152 billion in insured losses and $395 billion overall (i.e., insured plus uninsured, and including non-weather-related losses). Insured losses make up ~38% of the overall 2025 total, with the table below showing a regional breakdown for Average Annual Loss (AAL), and 1% and 0.4% loss estimates.

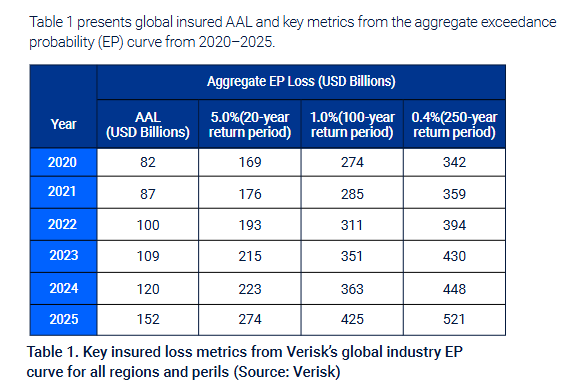

These loss estimates are not fixed. They change as the world changes — more people, more wealth, more exposure means more potential for loss. The table below from the Verisk shows how annual insured loss estimates have changed from 2020 to 2025. Have a look at the white column on the left, which reflects their estimated Average Annual Loss for each year from 2020 to 2025.

The AAL shows that expected losses increase by 50% from 2022 to 2025, from $100 billion to $152 billion, and almost doubled from 2020. Similarly, the levels of extreme losses have increased rapidly as well, with a loss with an estimated 1% chance in 2025 at $425 billion, representing an increase of $151 billion since 2020.

What is driving this remarkable increase in loss potential?

Climate change, obviously.

Right?

Wrong.

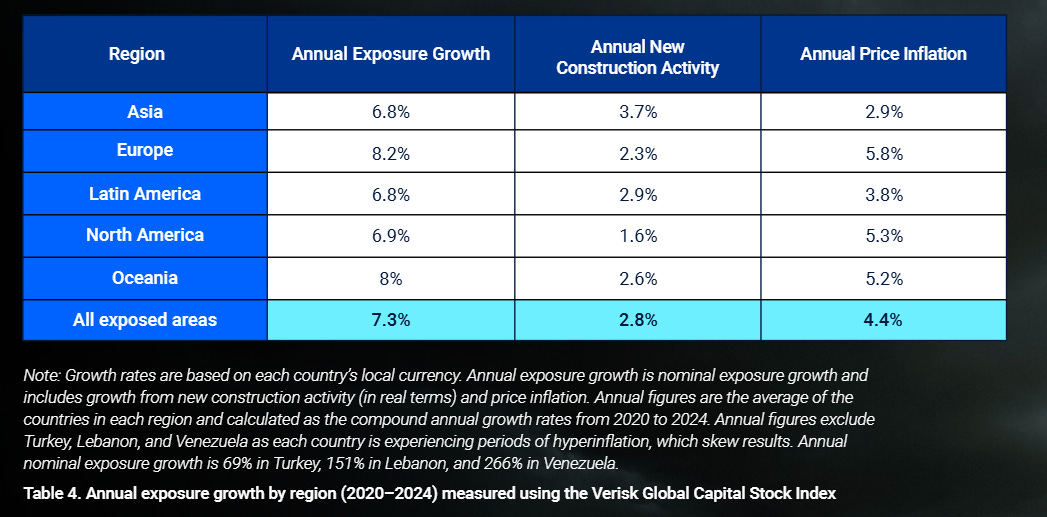

Verisk explains that increasing exposure to loss is being driven by construction and inflation [3]:

Insured losses—and the modeled AAL—increase over time in part because of growth in exposure to natural catastrophes. Over the past five years (2020–2024), global property exposure in Verisk-modeled countries grew about 7% per year on average (Table 4 [above]), driven by both new construction and construction price increases. Since 2020, fast-rising global inflation significantly increased exposure values, which in turn helped spur increases in insured natural catastrophe losses. While construction price inflation has slowed recently, exposure growth continues to contribute to rising insured losses.

Global loss estimates for 2025 have been reported in recent weeks by several reinsurance companies, allowing an update of my global time series of weather-related catastrophe losses through 2025. [4]

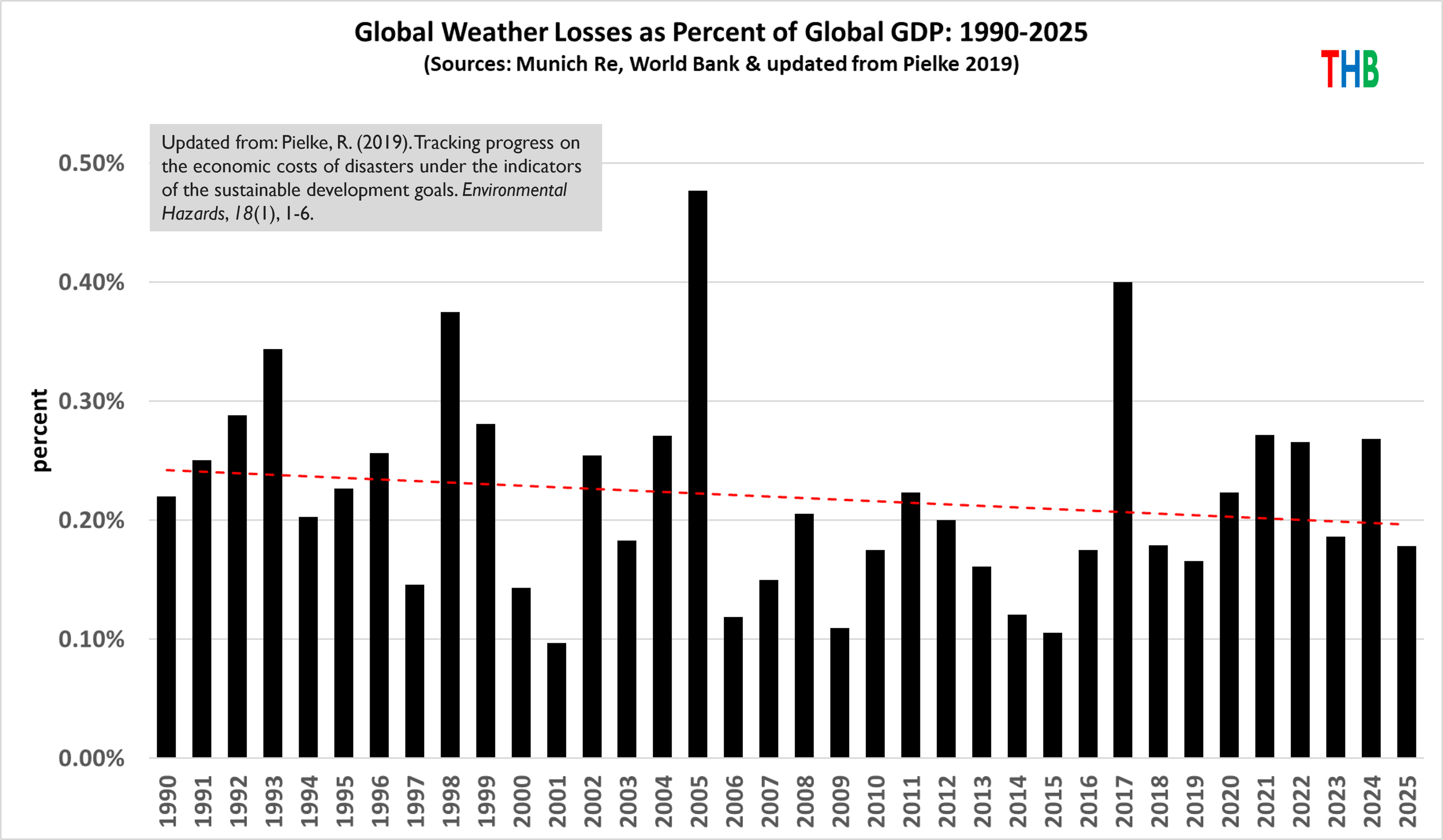

Munich Re, a global reinsurance company, has explained that they consider their time series of losses to be reliable since 1990. In my analyses, I use their data (along with GDP estimates from the World Bank) and in the figure below update the analysis of Pielke (2019) through 2025. [5]

The time series shown below shows total weather-related catastrophe losses as a percentage of global GDP (constant 2025 PPP dollars) for 1990 through 2025. [6] The data is freshly updated with the 2025 loss estimates from Munich Re, which estimates total weather-related losses for 2025 of $212 billion of which, $106.5 billion was insured. [7]

Last year’s losses as a percentage of GDP were ~0.18%, which were below both the long-term annual average of 0.22%, as well as the long-term linear trend (dashed red line) which since 1990 has fallen from ~0.25% to ~0.20% per year. [8]

In terms of absolute numbers, Munich Re’s estimates of $212 billion (total) and $106.5 billion (insured) are far below the Verisk 2025 AAL estimates of $152 billion (total) and $395 billion (total) — which include non-weather-related losses.

That means that weather-related losses for 2025 were well below expected annual loss totals in both absolute numbers and with respect to GDP — adding to a longer term trend of no increase in weather-related catastrophe losses as a proportion of GDP.

This is good news indeed! Even so, extremely large loss years are possible (even more than $1 trillion). Continuing progress on holding disaster losses in check and reducing other human impacts will require concerted, collective effort.

Meantime, Munich Re also expects to report €6.0 billion in profit for 2025 and projects profits of €6.3 billion for 2026.

Press on Climate Change! Press on!

[1] This analysis does not consider earthquakes or other non-weather-related losses, but the overall story is very much the same with those included in the data.

[2] There is nothing special about the Verisk estimates, other than the fact that they are relased to the public. Other firms provide such estimates as well, but almost all are held as proprietary. There is some variation across the estimates that I have seen, but the picture that they collectively paint is consistent.

[3] In actuarial departments in the re/insurance industry, there is absolutely no controversy over what factors are driving increasing loss potentials, despite what we read in the major media. Someone tell the New York Times.

[4] I discuss loss data quality in detail at this THB post. There is considerably more variation in total loss estimates than insured, because companies are required by law to accurately represent the latter whereas the former are estimates.

[5] To poke some fun at the weather truthers, I think I’m supposed to say that I am using “peer reviewed methods”!

[6] The United Nations, under its Sendai Framework for Disaster Risk Reduction recommends disaster losses as a percentage of GDP and an appropriate metric of progress with respect to quantifying the economic impacts of disasters.

[7] Munich Re includes in their 2025 totals $12 billion in total losses and $1.5 billion in insured for the March 2025 earthquake that struck Mynamar and neighboring countries. I have removed these losses from the totals, as they are not weather-related.

[8] The trend is real, but I do not view it to be predictive out of sample and into the future.

[9] I sound like a broken record, I know — If you want to look for signals of changes in climate, look at climate data, not economic loss data. Duh.