Part 1 of the THB series on climate change and insurance focused on the recent financial performance of the insurance industry in the context of fevered claims of its looming collapse due to climate-fueled extreme events.

Today, in Part 2 I take a deeper dive into one of the issues alluded to in that post — the rise of a climate-risk industrial complex in the global financial community.

Today’s installment looks at three issues:

The Invention of a New Type of Risk: “Climate Risk”

“Climate Risk” is Measured in the Economic Costs of Extreme Weather

Claim: The Past Says Little About “Climate Risk,” thus We Need New Risk Models

In short — The global financial community adopted a bespoke definition of “climate risk,” presented as a novel type of risk that could threaten the entire global financial system. Consequently, the argument went, regulators faced an imperative in developing new requirements for financial institutions to disclose their “climate risk” and creating of new regulations to govern that risk. Because “climate risk” was deemed to be newly emergent, the argument continued, new tools beyond conventional climate science were needed to measure and quantify that risk. The result has been the rise of a climate-risk industrial complex.

The Invention of New Type of Risk: “Climate Risk”

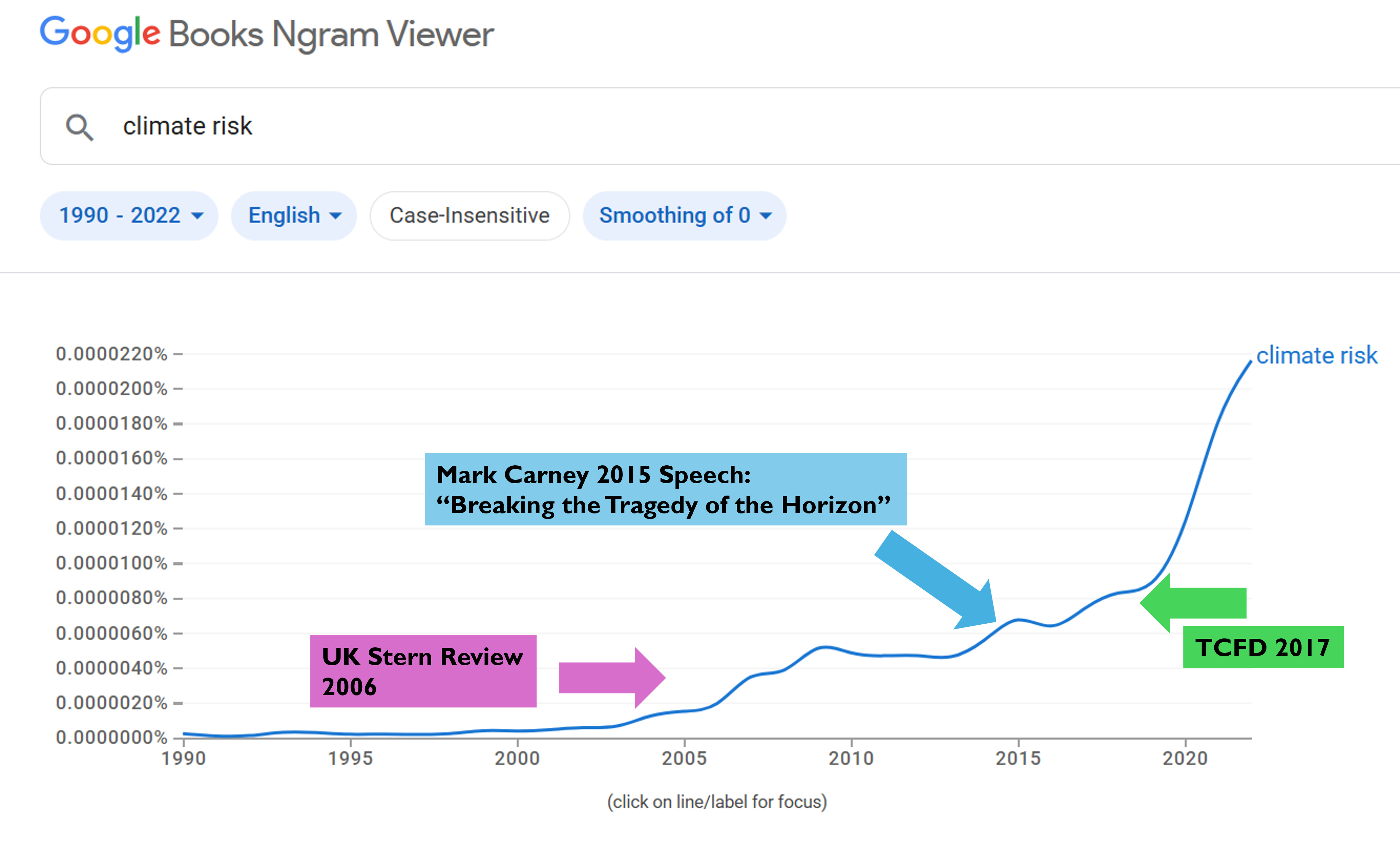

The notion of “climate risk” can be found sparingly in the literature prior to Mark Carney’s 2015 speech that launched the climate-risk industrial complex. The figure below, via Google Ngrams, shows the occurrence of the phrase “climate risk” in English language books published from 1990 to 2022.

The term was not much found prior to 2000, and subsequently followed a hockey stick pattern into the 2020s.

The TCFD classified “climate risk” into two categories, which became commonly adopted throughout the financial community:

(1) risks related to the transition to a lower-carbon economy and (2) risks related to the physical impacts of climate change.

The focus of today’s post is on the latter — physical risks.

The Financial Stability Board (FSB) — which oversaw the TCFD — was created in 2009 by the G20 in the aftermath of the Global Financial Crisis, and is hosted in Switzerland by the Bank for International Settlements (BIS, a consortium of central banks). The FSB exists to identify systemic risks in the global financial system and to make recommendations to regulators about possible actions in response. [2]

”[T]he possibility that the economic costs of the increasing severity and frequency of climate-change related extreme weather events, as well as more gradual changes in climate, might erode the value of financial assets, and/or increase liabilities.”

“[C]limate catastrophes are even more serious than most systemic financial crises: they could pose an existential threat to humanity, as increasingly emphasized by climate scientists (eg Ripple et al (2019)).”

It is jarring to come across a reference to Ripple et al. 2019 — a neo-Malthusian catastrophist article at odds with the Intergovernmental Panel on Climate Change (IPCC) — in a report of the typically staid BIS.

Here is an short excerpt from Ripple et al.:

“Profoundly troubling signs from human activities include sustained increases in both human and ruminant livestock populations . . . the world population must be stabilized—and, ideally, gradually reduced—within a framework that ensures social integrity.”

Either the global financial community swallowed the notion of catastrophic climate change hook, line, and sinker — or, more cynically, it put apocalyptic visions to work as a tool to try to reengineer the entire global economy. Either way, mainstream climate science was left far behind.

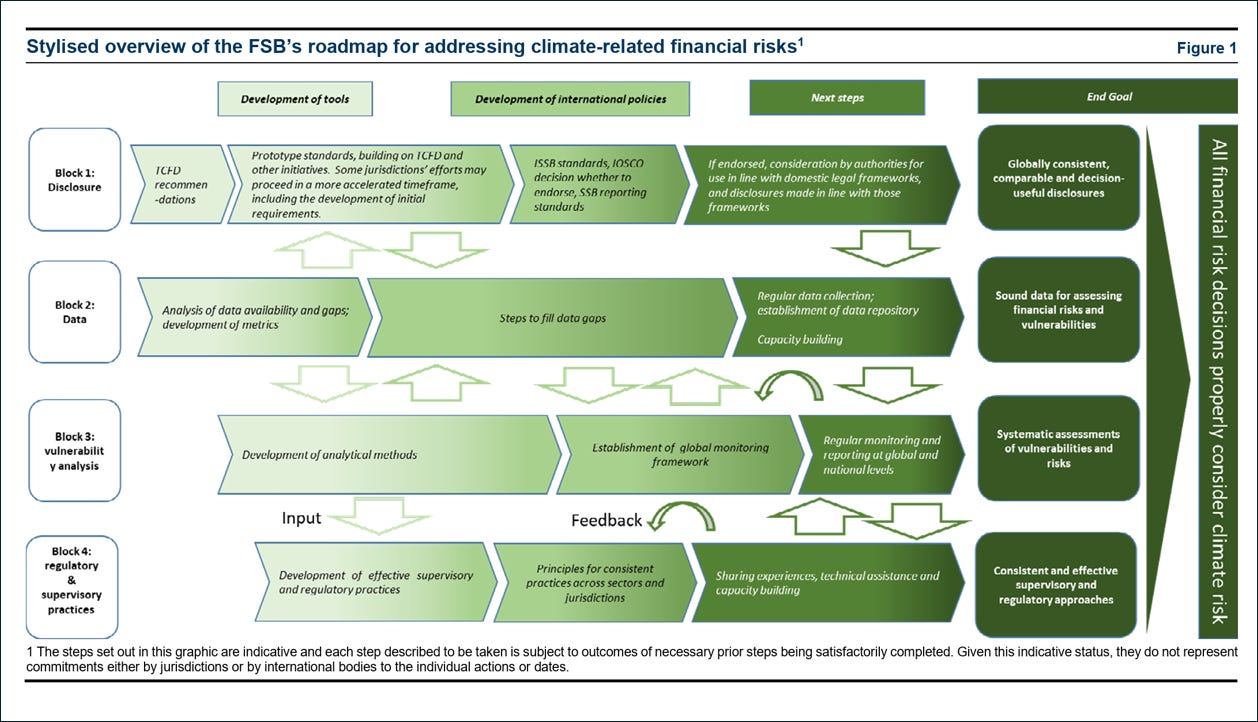

In 2021, the FSB produced a “roadmap for addressing climate-related financial risks.” That “roadmap,” summarized in the figure below from that report, provides the justification for the creation of an ecosystem of new institutions to address “climate risk” in finance.

I have named the resulting panoply of new institutions the “climate-risk industrial complex” for the simple reason that there is no such thing as novel physical “climate risk.”

Changes in the frequency and intensity of weather metrics are of course real, and the detection and attribution (to human causes) of change has, for some phenomena, occurred, according to the IPCC.

But there is no such thing as newly emergent “climate risk” to be managed separately from the ongoing risks associated with hurricanes, floods, tornados, etc., whose incidence may change and vary on all time scales, and for many reasons, including but not limited to human influences.

The establishment of a climate-risk industrial complex was thus unnecessary. Beyond that, its existence is justified by a wholesale rejection of mainstream climate science as well as longstanding practices for managing the impacts of weather and climate on society.

“Climate Risk” is Measured in the Economic Costs of Extreme Weather

The financial community has routinely measured physical climate risks in terms of the economic costs associated with extreme weather, and in the process, often (mistakenly) conflating trends in losses with trends in extreme weather.

“Physical impacts are not just risks for the future; they are already impacting the economy and financial system today. Overall, worldwide economic costs from natural disasters have exceeded the 30-year average of USD 140 billion per annum in 7 of the last 10 years. Since the 1980s, the number of extreme weather events has more than tripled.”

Note how in that last sentence the NGFS incorrectly uses the trend in losses to make a conclusion about “extreme weather events.” The data relied on by the NGFS in the passage above comes from the global reinsurer, Munich Re, whose data on catastrophe losses I have studied extensively for decades (e.g., here, here, here, here).

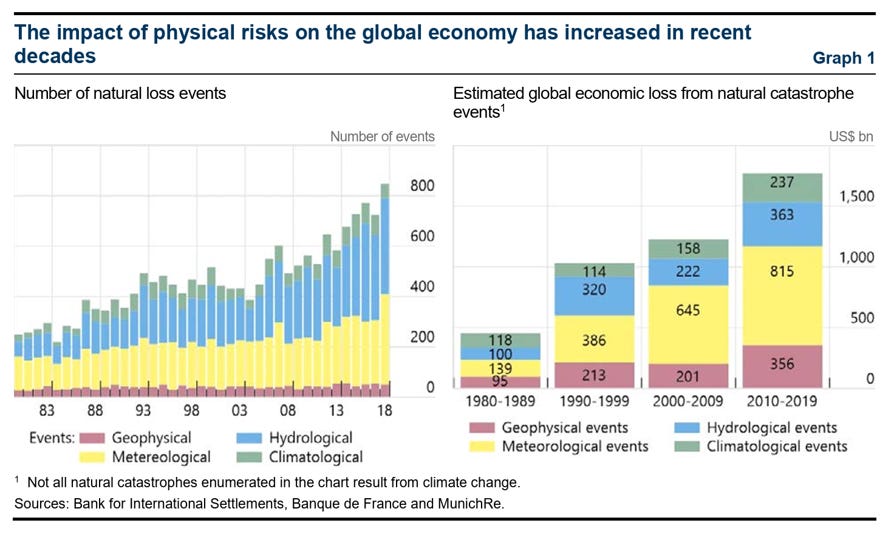

Munich Re data shows up everywhere. For instance, the FSB, in its 2020 report, The implications of climate change for financial stability, cites Munich Re loss data to claim that the “physical risks” of climate change have increased:

“Economic losses from natural catastrophes have increased in recent decades. The number of some types of extreme weather events globally has steadily increased (Graph 1, LH panel). The weight of scientific evidence suggests that such events have become more likely or more severe due to the anthropogenic effects of climate change, and that further anthropogenic warming will cause them to intensify. Economic losses associated with such events have also increased (Graph 1, RH panel).”

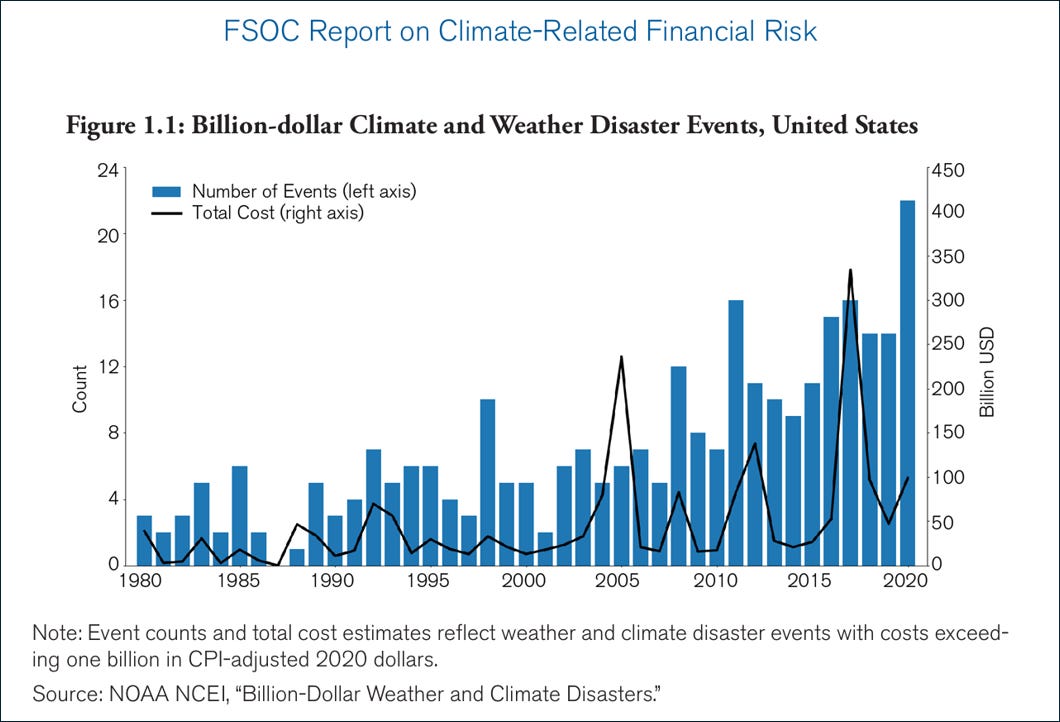

In the United States, the preferred dataset to indicate the “physical risks” of climate change was — of course — the “Billion Dollar Disaster” tabulation of the National Oceanic and Atmospheric Administration (NOAA).

For instance, the U.S. Financial Stability Oversight Council (FSOC), also created in the aftermath of the Global Financial Crisis, in 2021 identified “Climate Change as a Threat to Financial Stability.”

It is no exaggeration to conclude that the primary justification for the emergence of the climate-risk industrial complex are claims of escalating climate-fueled disaster losses based on Munich Re’s disaster loss data and NOAA’s Billion Dollar Disaster tabulation, two topics I’ve studied for decades.

I’m starting to understand much better why my research on disasters and climate change has attracted so much attention!

Claim: The Past Says Little About “Climate Risk,” thus We Need New Risk Models

One big problem for the climate-risk industrial complex is that mainstream, consensus science does not support the notion of novel “climate risk.” You don’t need to take it from me and my colleagues — Take it from the IPCC.

Perhaps because the IPCC does not offer much in the way of support for novel physical “climate risk,” the financial community has taken a stance that climate data from the past is simply irrelevant to current and near-terms risks of climate change.

Instead, the financial community claims that we now need a new type climate science focused on “climate risk” and implemented largely by private sector consultants.

For instance, in 2021 the TCFD argued that climate data from the past cannot provide a reliable guide to current and future risks:

“Data on past changes in climate may also be a particularly poor guide to future climate-related risks to the financial system. This is because future changes in the drivers of climate-related risks may be non-linear, and prone to rapid acceleration. Increases in global temperatures may also be subject to positive feedback effects, as they could prompt an increase in emissions levels that themselves cause further increases in temperatures. This reduces the degree to which historical trends can serve as a guide to the future magnitude and dynamics of climate-related risks.”

The BIS in 2020 made a similar argument, arguing that “climate risk” management requires a fundamentally new approach to evaluating climate risks:

“[T]raditional approaches to risk management consisting in extrapolating historical data and on assumptions of normal distributions are largely irrelevant to assess future climate-related risks. That is, assessing climate-related risks requires an “epistemological break” (Bachelard (1938)) with regard to risk management . . .”

The “epistemological break” referred to here means a departure from conventional climate science — such as the IPCC’s framework for detection and attribution — to more directly connect greenhouse gas emissions with disaster losses.

In 2017, the TCFD explained that meant repurposing climate scenarios (such as our old friend, RCP8.5) and creating new types of risk models to assess near-term “climate risk”:

“Organizations may decide to use existing external scenarios and models (e.g., those provided by third-party vendors) or develop their own, in-house modeling capabilities.”

The consequence has been the emergence of a new ecosystem of “climate risk” vendors who promise the ability to accurately quantify the impacts of climate change, today and tomorrow, on individual properties anywhere in the world.

This new science-like ecosystem of “climate risk” has been profoundly consequential:

“[R]isk estimates from analytics companies are likely to affect billions of lives and trillions of dollars”

That’s where Part 3 begins in the next installment of the series.

Read more about the “climate-risk institutional complex” from Jessica Weinkle: